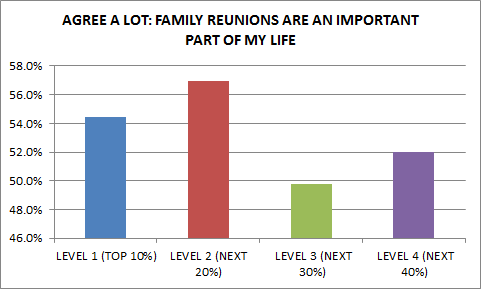

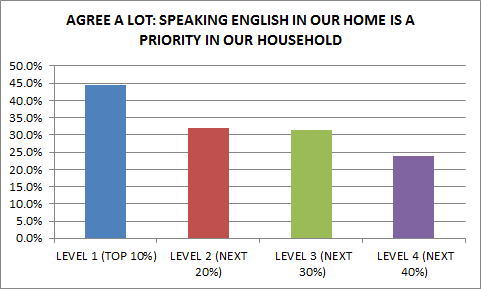

Using data from the Experian Simmons National Hispanic Consumer Study that was collected in the twelve months ending on August 31, 2012, I created crosstabulations of the TGI Socio Economic Scale in the Simmons database by preference to watch television “Only in English,” “Mostly in English but Some in Spanish,” “Mostly in Spanish but Some in English,” and “Only in Spanish.” The television language preference variable in the analysis combined those who watch “Only in English” and “ Mostly in English but Some in Spanish” in one group, and those who watch in “Only in Spanish” and “Mostly in Spanish but Some in English” in another group. Respondents stated their preference when reacting to the statement “When you watch television do you prefer to watch television programs...” The TGI Socio Economic Scale is a composite of education, ownership of selected household durables, mobile phone ownership, credit card ownership, usage of Internet and air travel. The scale results in four levels of socioeconomic standing: The top 10% of the population, the next 20% of the population, the next 30% of the population, and finally the remaining 40%.

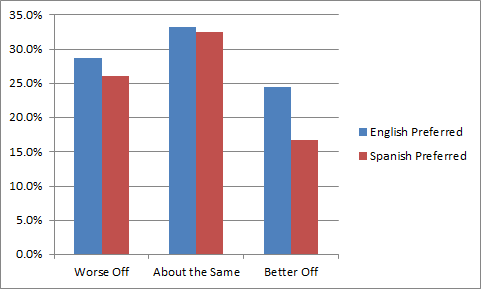

The following line chart illustrates the trends uncovered:

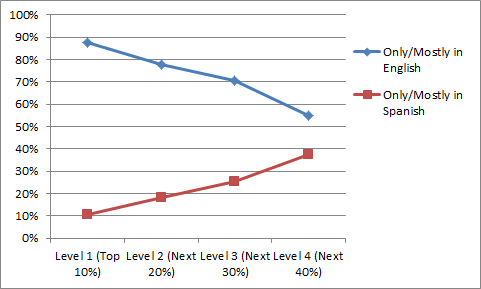

As can be observed, the lowest socioeconomic level of Latinos is more likely than anyone else to prefer watching television in Spanish, although a substantive percentage of them also indicate preferring only English or mostly English television exposure. The percentages of Hispanics at this lowest level are more equally divided among language preferences than for any other socioeconomic level. Those in Level 3 are more polarized than the lowest level as their percentages are more divided between the two languages. The polarization increases at Levels 1 and 2 as they are more dramatically divided and in the large majority they prefer television exposure in the English language.

Overall, there is a tendency for those better educated and more affluent to prefer television in the English language and for those who are in the lower levels to be more oriented to the Spanish language. It is also likely that those in the higher socioeconomic levels are more acculturated into the US. The tendencies are almost linear and monotonic.

These trends point to the dynamics of the Latino market and its complexity. While the preference to watch programming in the Spanish language continues to be important for a substantive portion of the Latino population, it is not a uniform tendency. This is clearly due to the fact that with so many channels in English, Latinos simply find more offerings in English than in Spanish. It is likely that the diversity of content in English drives some of these trends. Those more affluent can be expected to have more choices of channels for the enjoyment of television programming and that may explain some of these preferences. Also, at the lower levels there are those who have been born in the United States that share their socioeconomic level with newer immigrants. That makes for an interesting mix of acculturation stages that affect television language preferences.

Further, as Latinos become more able to appreciate content in English, their content horizons seem to expand. Socioeconomic status and bilingualism and English fluency are related.

Marketers can take from these findings important lessons and cautions:

1. Media planning is not straightforward. Socioeconomic level plays a role and thus different types of products may do better on English language television platforms, and others on Spanish.

2. A mix of language television platforms may be appropriate for many advertising campaigns as television language preferences, particularly at Levels 3 and 4, are more divided. They represent 70% of the Latino population.

3. Language preference for television watching may not be indicative of assimilation but of content availability and content preferences. Thus cultural insights should likely drive marketing and advertising campaigns.

This data confirms the diversity and complexity of the Latino market and the importance of sophisticated media planning efforts.

The data used here is from the Experian Simmons National Hispanic Consumer Study and was collected from August 1, 2011 to August 31, 2012. The sample contained 8120 Latinos.